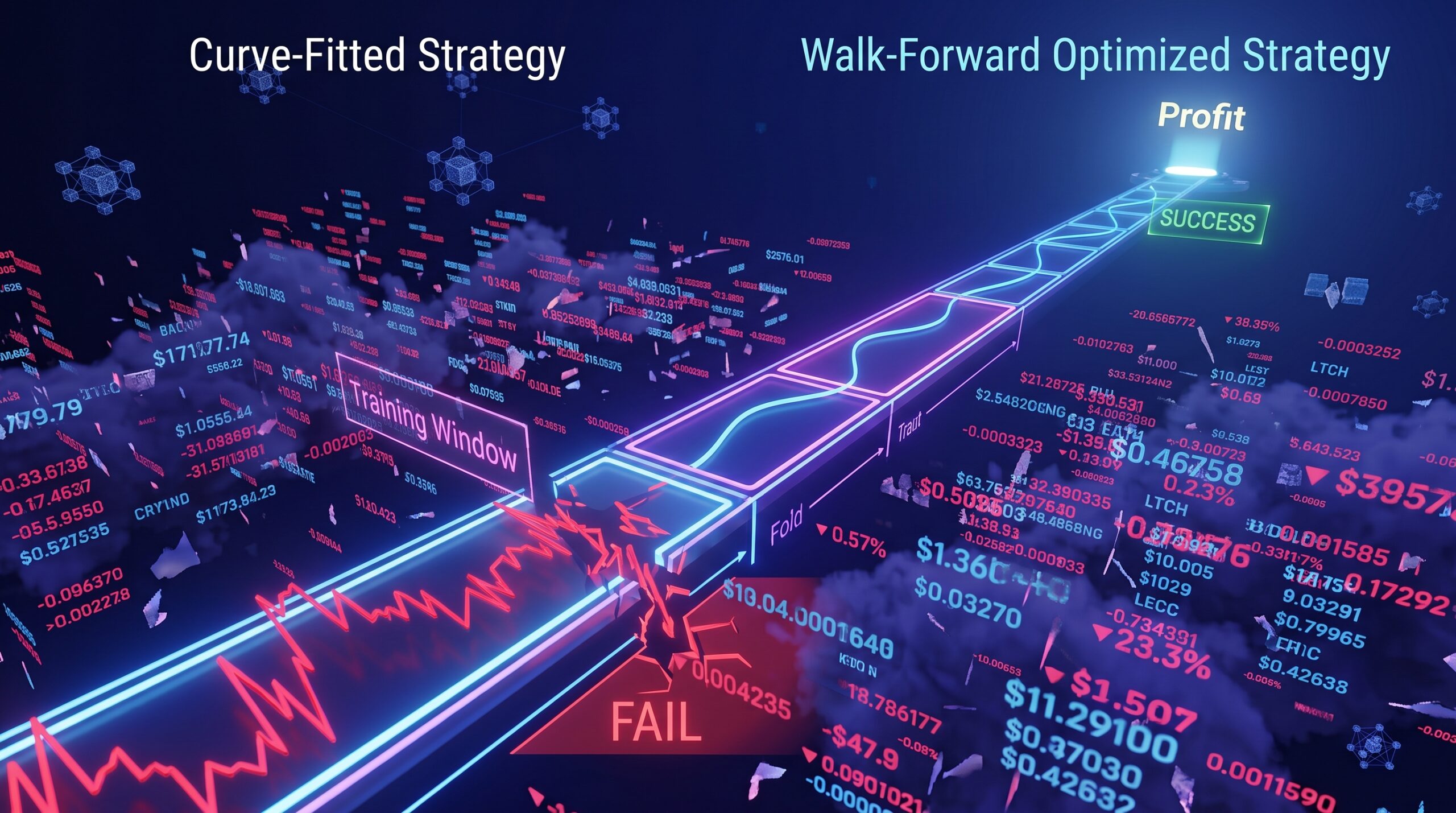

You have likely built a trading strategy, spent weeks tweaking the parameters, and finally achieved a backtest with a beautiful, upward-sloping equity curve. You deploy it, feeling invincible, only to watch it collapse the moment it hits live market data. We have all been there. It is the classic “curve-fitting” trap: you have inadvertently taught your bot to memorize the past rather than understand the market’s underlying mechanics.

The crypto market is far too volatile for “static” strategies that rely on hard-coded history. To build a bot that actually survives the unpredictable churn of 2026, you need to abandon standard backtesting in favor of walk-forward testing. This is the only way to ensure your strategy is adaptive rather than just a historical artifact. Let’s look at how to build a testing pipeline that keeps your capital safe.

Understanding the Curve-Fitting Trap

Curve-fitting happens when you optimize your bot’s parameters—like RSI thresholds or moving average lengths—to perfectly match a specific period of historical data. Your bot looks like a genius on paper because it knows exactly when the 2023 bull run started and exactly when the 2024 crash occurred. Once you move to live trading, that “perfect” fit becomes a liability because the market never repeats the exact same sequence twice.

Expert Insight: If your strategy performs significantly better in the backtest than it does in “out-of-sample” testing, you are over-fitted. Real strategies should be slightly “messy” and robust. If your equity curve is too smooth, you have likely optimized away the natural randomness of the market, which is the first sign of a failure waiting to happen.

The Walk-Forward Framework

Walk-forward testing is the professional solution to this problem. Instead of testing over one giant data block, you divide your data into a series of “windows.” You optimize your bot on an “in-sample” period (e.g., three months), then test it on an “out-of-sample” period (e.g., the following month). You then “walk forward” the entire process by moving your window one month at a time.

Personal Example: I used to optimize my mean-reversion bot on a full year of data. It looked perfect, but failed every time the market regime shifted. Now, I use a rolling 60-day optimization window followed by a 15-day out-of-sample test. My bot is constantly “re-learning” the current market conditions. It feels less “perfect” than my old strategy, but it is infinitely more reliable because it isn’t trying to force the future to look like the past.

Balancing Adaptability and Stability

The goal of walk-forward optimization isn’t to change your bot’s core logic every week. It is to fine-tune the sensitivities of your parameters. You want your strategy to be “stationary,” meaning the core logic holds up across different regimes, but the parameters breathe with the market.

Expert Insight: When you walk forward, monitor the “parameter drift.” If your optimal moving average length shifts from 10 to 200 in the span of a month, your strategy is unstable and fundamentally flawed. A robust strategy should see its parameters shift only slightly. If the parameters are swinging wildly, your strategy is not capturing a market truth; it is just reacting to noise.

Avoiding Common Testing Pitfalls

One of the biggest mistakes in bot testing is ignoring transaction costs and slippage. In a backtest, your bot might make a profit on 0.01% price moves. In reality, exchange fees and spread will eat that profit instantly. Your walk-forward test must include a “realistic commission” variable. If your bot is profitable only when commissions are zero, it is not a trading strategy—it is a math error.

Expert Insight: Always run a “Monte Carlo” simulation after your walk-forward testing. This process randomly shuffles your historical trades to see if your strategy can survive a string of bad luck. If a random reshuffling of your trades results in bankruptcy, your strategy is too fragile, no matter how good the walk-forward results look.

Walk-forward testing is the difference between a hobbyist script and a professional trading system. By constantly testing your bot against unseen data, you force it to adapt to the market’s changing moods rather than relying on the ghosts of historical bull runs. Stop chasing the “perfect” backtest, start building for robustness, and ensure your bot is designed to handle the unknown. The market doesn’t care about your past results—it only cares about your ability to adapt to the next move.

FAQ

How often should I walk-forward test my bot? It depends on your timeframe. If you are a scalper, you might need to re-optimize every few days. If you are a swing trader, a monthly walk-forward cycle is usually sufficient.

Does walk-forward testing eliminate all risk? No. It drastically reduces the risk of curve-fitting, but it cannot predict “Black Swan” events or structural market changes that haven’t occurred before.

What software is best for this? You can implement walk-forward testing in Python using libraries like pandas and scikit-learn, or use professional backtesting platforms that support “rolling” optimization windows.

What is the “Out-of-Sample” (OOS) period? OOS data is data your bot has never seen during the optimization process. It is the “real-world” test that proves whether your strategy actually works or if it’s just curve-fitted.